Hidden Leverage or Hidden Liability? What Private Equity and Family Offices Must Know About Multi-Tiered Entity (MTE) Structures

When a family office acquired a controlling interest in a boutique manufacturing business, everything on the surface looked clean. U.S.-based, profitable, and fully audited. But six months in, the CFO noticed inconsistencies between projected distributions and actual cash flows. What unfolded was a lesson in modern entity structuring: buried beneath the flagship company were five SPVs, an offshore IP holding subsidiary, and multiple intercompany loans that had never been formally documented.

Welcome to the world of Multi-Tiered Entities (MTEs), where the value isn’t just in the assets, but in the structure itself.

What Are MTEs?

Multi-tiered entities (MTEs) are layered legal structures where a parent company controls multiple levels of subsidiaries, SPVs (special purpose vehicles), and investment vehicles. They are ubiquitous in private equity portfolios, real estate investment platforms, and family office structures. These entities offer flexibility, tax efficiency, and asset protection—but they also introduce significant complexity in valuation, reporting, and compliance.

Why MTEs Pose Unique Risks to Investors

- Layered Ownership: Each tier creates a new layer of financial influence and control to be analyzed.

- Geographic Spread: Subsidiaries across jurisdictions are governed by different laws, tax policies, and disclosure rules.

- Intercompany Transactions: Cash sweeps, management fees, and IP licensing can distort earnings and make it difficult to trace the actual flow of funds.

“With MTEs, it’s not just about value—it’s about structure. A strong framework maps ownership, aligns reporting, and ensures tax compliance at every level.”

— Rose Araghchy, CPA, Founder & CEO, R2 Advisors PC

A Framework for Financial Clarity

- Define the Purpose – Valuation must reflect intent: tax, sale, dispute, or internal planning.

- Map Ownership in Full – Build a transparent, tier-by-tier diagram.

- Select the Right Valuation Method – Income, asset-based, or market approach should align with entity function.

- Assess Ownership Rights – Controlling vs. non-controlling interests impact value.

- Apply Strategic Discounts – Use DLOC and DLOM cautiously to avoid over-discounting across layers.

- Calculate Tier-by-Tier, Then Roll Up – Model value from the bottom up.

- Document Everything – You’ll need it for both internal review and IRS defensibility.

What Influences MTE Value?

- Lack of Control

- Illiquidity

- Voting Rights

- Ringfencing via SPVs

- Cross-Border Risks

- Cumulative Discounting

“In multi-tiered structures, the real risk isn’t complexity—it’s invisibility. Without a framework that surfaces intercompany flows, jurisdictional mismatches, and control dynamics, tax and reporting decisions are built on assumptions, not facts.”

— Rose Araghchy, CPA, Founder & CEO, R2 Advisors PC

The Legal and Regulatory Terrain

Family offices and PE firms must also account for:

- Legal Precedent: Discount stacking and SPV transparency are hot areas for IRS scrutiny.

- Jurisdictional Variance: Reporting rules vary widely between U.S., Cayman, Luxembourg, and beyond.

- Compliance Burden: Transfer pricing, BEPS, and entity-level tax rules increase audit exposure.

Industry Applications

| Industry | Application of MTEs |

|---|---|

| Private Equity | Foundational in fund structuring, SPVs, and co-investments |

| Real Estate | Uses SPVs to ringfence risk; makes consolidated valuation complex |

| Technology & IP | Heavy on intangibles; requires specialized models for cross-border licensing and valuation |

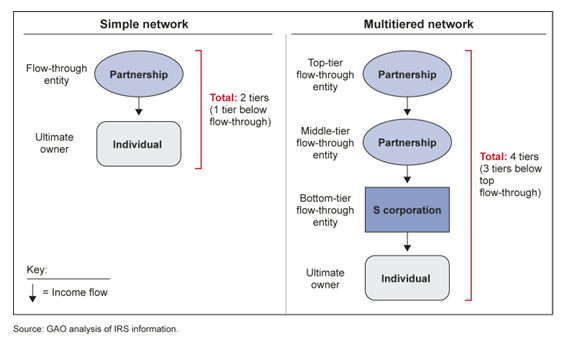

MTE Structure Comparison: Simple vs. Complex Layered Entities